All Categories

Featured

Table of Contents

In exchange for earning a limited quantity of the index's growth, the IUL will never ever get less than 0 percent rate of interest. Also if the S&P 500 declines 20 percent from one year to the following, your IUL will certainly not shed any kind of cash money worth as an outcome of the market's losses.

Envision the passion compounding on an item with that kind of power. Given all of this information, isn't it possible that indexed global life is a product that would permit Americans to acquire term and spend the rest?

A real financial investment is a protections item that goes through market losses. You are never ever subject to market losses with IUL just since you are never based on market gains either. With IUL, you are not spent in the market, but merely gaining passion based on the efficiency of the market.

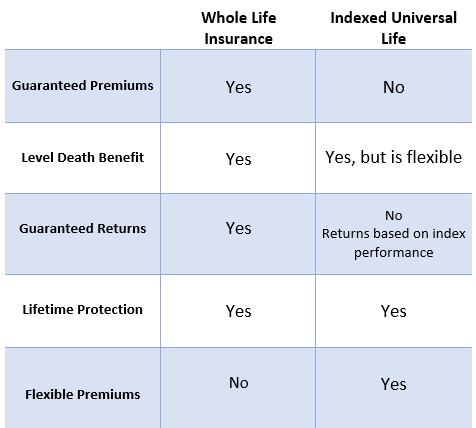

Returns can expand as long as you remain to make payments or keep a balance. Compare life insurance policy online in minutes with Everyday Life Insurance. There are two types of life insurance: permanent life and term life. Term life insurance policy only lasts for a particular duration, while permanent life insurance coverage never ends and has a money worth component along with the survivor benefit.

New York Life Variable Universal Life Accumulator

Unlike universal life insurance policy, indexed global life insurance policy's cash money value gains interest based on the performance of indexed stock markets and bonds, such as S&P and Nasdaq., points out an indexed universal life policy is like an indexed annuity that really feels like global life.

Due to these functions, long-term life insurance policy can work as a financial investment and wealth-building device. Universal life insurance was produced in the 1980s when rates of interest were high. Like other kinds of permanent life insurance policy, this plan has a cash money worth. Universal life's cash value makes passion based upon current money market rates, but rate of interest change with the marketplace.

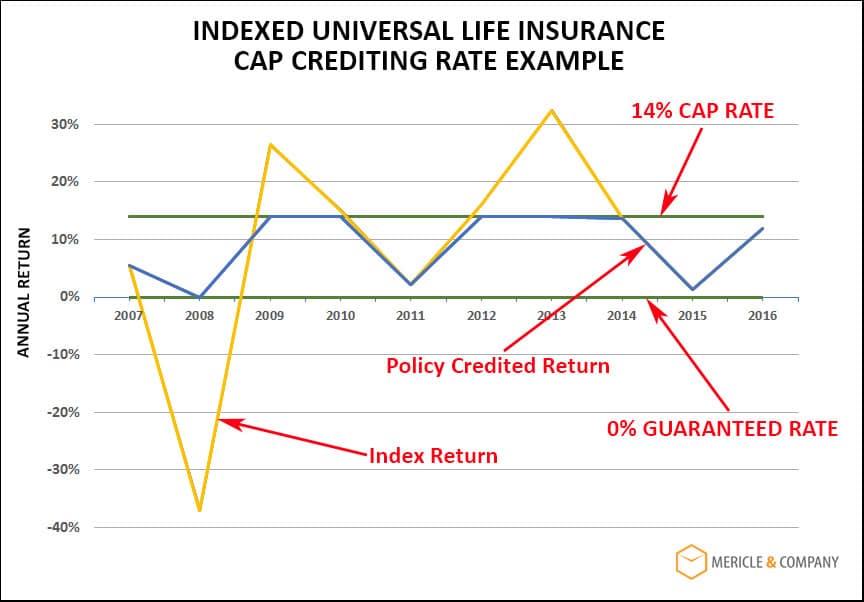

Indexed universal life plans supply a minimal surefire interest rate, likewise recognized as an interest attributing floor, which decreases market losses. State your cash money worth sheds 8%.

Books On Indexed Universal Life

It's additionally best for those ready to assume extra risk for higher returns. A IUL is a long-term life insurance coverage policy that obtains from the properties of a global life insurance policy. Like global life, it allows versatility in your survivor benefit and premium settlements. Unlike universal life, your cash money worth grows based on the efficiency of market indexes such as the S&P 500 or Nasdaq.

Her job has been published in AARP, CNN Highlighted, Forbes, Lot Of Money, PolicyGenius, and U.S. Information & Globe Report. ExperienceAlani has reviewed life insurance policy and pet dog insurer and has written countless explainers on travel insurance policy, credit scores, financial obligation, and home insurance. She is enthusiastic regarding debunking the complexities of insurance and various other personal finance topics to make sure that visitors have the details they require to make the very best money choices.

Paying only the Age 90 No-Lapse Premiums will certainly ensure the fatality benefit to the insured's attained age 90 but will certainly not assure money worth buildup. If your customer ceases paying the no-lapse guarantee premiums, the no-lapse attribute will certainly terminate prior to the guaranteed period. If this happens, added premiums in an amount equivalent to the shortfall can be paid to bring the no-lapse feature back effective.

I recently had a life insurance sales person turn up in the remarks thread of a message I released years ago regarding not mixing insurance coverage and investing. He thought Indexed Universal Life Insurance (IUL) was the best thing given that cut bread. On behalf of his placement, he posted a web link to an article composed in 2012 by Insurance Coverage Representative Allen Koreis in 2012, entitled "16 Reasons Accountants Prefer Indexed Universal Life Insurance Policy" [web link no longer available]

Indexed Life Insurance Pros Cons

First a quick explanation of Indexed Universal Life Insurance Policy. The destination of IUL is evident. The property is that you (practically) get the returns of the equity market, without any kind of risk of shedding cash. Currently, prior to you diminish your chair making fun of the absurdity of that declaration, you require to understand they make a very convincing debate, a minimum of until you take a look at the details and realize you do not get anywhere near the returns of the equity market, and you're paying much excessive for the assurances you're obtaining.

If the market goes down, you get the guaranteed return, typically something between 0 and 3%. Obviously, given that it's an insurance plan, there are likewise the common expenses of insurance, commissions, and surrender costs to pay. The details, and the factors that returns are so dreadful when mixing insurance coverage and investing in this particular way, come down to primarily three things: They just pay you for the return of the index, and not the returns.

Universal Aseguranza

If you cap is 10%, and the return of the S&P 500 index fund is 30% (like last year), you get 10%, not 30%. If the Index Fund goes up 12%, and 2% of that is returns, the modification in the index is 10%.

Include all these effects with each other, and you'll discover that lasting returns on index universal life are pretty darn near those for whole life insurance policy, positive, yet reduced. Yes, these plans assure that the cash money value (not the cash that goes to the prices of insurance policy, naturally) will not shed money, however there is no guarantee it will certainly maintain up with rising cost of living, much less expand at the price you need it to expand at in order to supply for your retired life.

Koreis's 16 factors: An indexed universal life policy account value can never ever lose cash due to a down market. Indexed global life insurance coverage assurances your account worth, securing in gains from each year, called a yearly reset.

In investing, you make money to take threat. If you do not wish to take much danger, do not expect high returns. IUL account worths grow tax-deferred like a qualified plan (IRA and 401(k)); shared funds do not unless they are held within a certified plan. Put simply, this implies that your account value benefits from three-way compounding: You earn interest on your principal, you earn passion on your interest and you make interest accurate you would certainly or else have actually paid in tax obligations on the rate of interest.

Nationwide Iul Review

Although certified plans are a far better option than non-qualified plans, they still have issues absent with an IUL. Investment choices are generally restricted to shared funds where your account value goes through wild volatility from direct exposure to market threat. There is a large distinction in between a tax-deferred pension and an IUL, but Mr.

You buy one with pre-tax dollars, reducing this year's tax bill at your limited tax rate (and will certainly often have the ability to withdraw your money at a reduced reliable price later) while you purchase the various other with after-tax bucks and will be forced to pay rate of interest to obtain your very own cash if you do not intend to surrender the plan.

He tosses in the timeless IUL salesperson scare tactic of "wild volatility." If you dislike volatility, there are far better methods to decrease it than by purchasing an IUL, like diversification, bonds or low-beta stocks. There are no restrictions on the amount that might be added annually to an IUL.

That's comforting. Let's think of this momentarily. Why would the federal government put limits on just how much you can put right into retirement accounts? Perhaps, simply maybe, it's since they're such a lot that the federal government doesn't want you to conserve too much on tax obligations. Nah, that couldn't be it.

{kind=link}

Latest Posts

Universal Insurance Payment

Universal Vs Term Insurance

Is An Iul A Good Investment